Why Speed Matters in Home‑Improvement Financing

.png)

Home‑improvement projects often require contractor financing solutions that can be initiated and completed while purchase intent is at its peak. Industry studies show that delays or unnecessary complexity in the financing workflow directly reduce application completions and, by extension, sales revenue. This article summarizes the current research on consumer tolerance for slow or tedious payment processes, highlights the heightened abandonment risk among younger consumers, and outlines measurable benchmarks for delivering an efficient, reliable financing experience. Companies exploring home improvement finance companies or developing customer financing for contractors must pay particular attention to these dynamics to stay competitive.

Consumer Expectations for Digital Financing

Digitally enabled shoppers expect the same speed and clarity from a financing application that they experience when placing ordinary retail orders. Across sectors, the following thresholds have emerged:

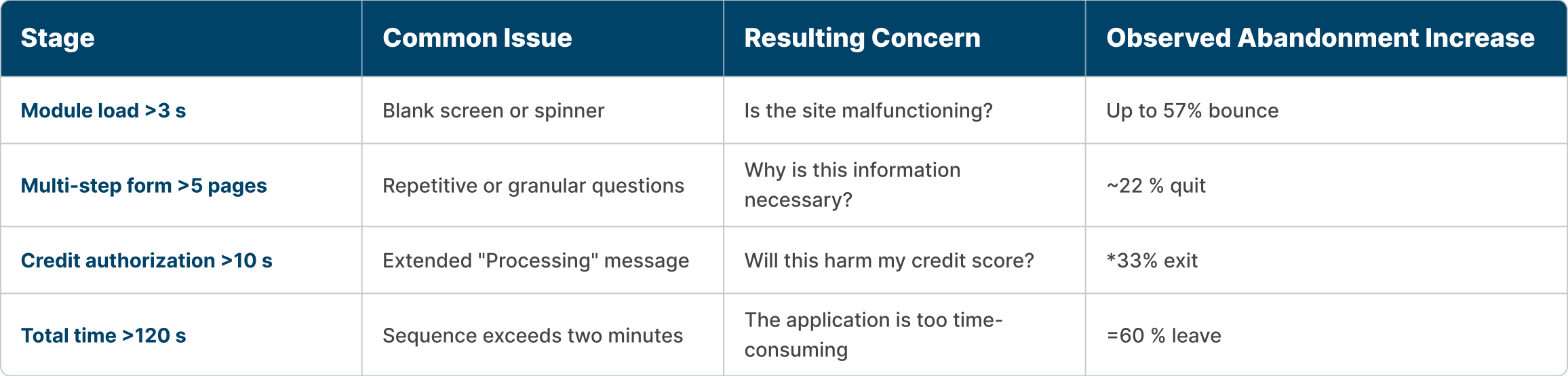

- Initial load time: Shoppers begin to question reliability once a financing module or embedded form takes more than 3 seconds to display. Abandonment can rise to 40–57 percent at this point. (source)

- Total application duration: Flows that extend beyond 30 seconds begin to lose up to half of prospective applicants. At two minutes, attrition can reach 60 percent.

- Form complexity: Each additional field or step increases cognitive load and perceived risk. Research from Baymard Institute indicates that keeping visible inputs to eight or fewer materially improves completion rates.

Speed therefore serves as both a practical convenience and a proxy for trust. A fast application signals technical competence, data security, and respect for the applicant’s time; a slow or erratic sequence communicates the opposite. For financing companies for contractors, ensuring a rapid and seamless experience can directly impact application completion rates and drive sales.

Key Psychological Drivers

Three well‑documented behavioral factors explain why consumers abandon slow financing flows:

- Progress Feedback: Users require evidence that the system is advancing. A visible progress indicator that updates in under ten seconds reinforces confidence. Stalled feedback erodes trust and lengthens perceived wait times.

- Effort–Reward Balance: Potential buyers weigh the value of completing the purchase against the perceived effort of the process. When effort outweighs benefit—particularly for discretionary upgrades—they exit the flow.

- Queue Visibility: In digital contexts, the number of form fields functions as a visible queue. Long forms signal longer waits and elevate anxiety—especially on mobile devices with limited screen real estate.

For businesses wondering how to offer financing to my customers construction, understanding these psychological drivers is critical to designing an effective, conversion-friendly financing flow.

Process Analysis: Typical Abandonment Points

These behaviors occur consistently across ticket sizes and product categories, underscoring the importance of continuous performance monitoring and optimization. Whether partnering with home improvement lenders for contractors or developing in-house programs, firms must design financing workflows that prioritize speed and simplicity.

Generational Differences in Abandonment Risk

Millennials and Generation Z currently represent the fastest‑growing share of U.S. homeowners and, consequently, a significant portion of home‑improvement spend. They also demonstrate markedly lower tolerance for friction:

- Higher mobile usage: Initial research indicates mobile abandonment rates near 86 percent for typical e‑commerce carts, with similar patterns in financing widgets displayed on smartphones.

- Greater sensitivity to delay: Comparative studies reveal that Millennials and Gen Zers abandon digital flows approximately seven times more frequently than Baby Boomers when confronted with slow response times or ambiguous form requests.

.png)

Any customer finance solution for contractors targeting this demographic must prioritize mobile‑first design, immediate system feedback, and concise data entry.

Performance Benchmarks for 2025

The following targets provide a practical framework for evaluating and improving financing workflows:

Organizations that consistently remain in the Green Zone realize higher approval and close rates, lower support costs, and stronger customer satisfaction scores. Offering the best contractor financing for customers becomes much more effective when these performance benchmarks are met.

Implementation Recommendations

- Pre‑populate data whenever possible. Passing name, address, and contact details from the shopping cart into the financing form eliminates redundant typing and reduces input errors.

- Provide real‑time status updates. Clearly labelled progress indicators and countdown timers reduce perceived wait times and discourage premature exits.

- Use soft credit pulls for preliminary decisions. This approach protects applicant credit scores and speeds up the initial response. A hard pull can be performed only upon acceptance of terms.

For companies offering customer financing software for contractors, these enhancements can significantly reduce friction and abandonment, ensuring a smoother customer journey.

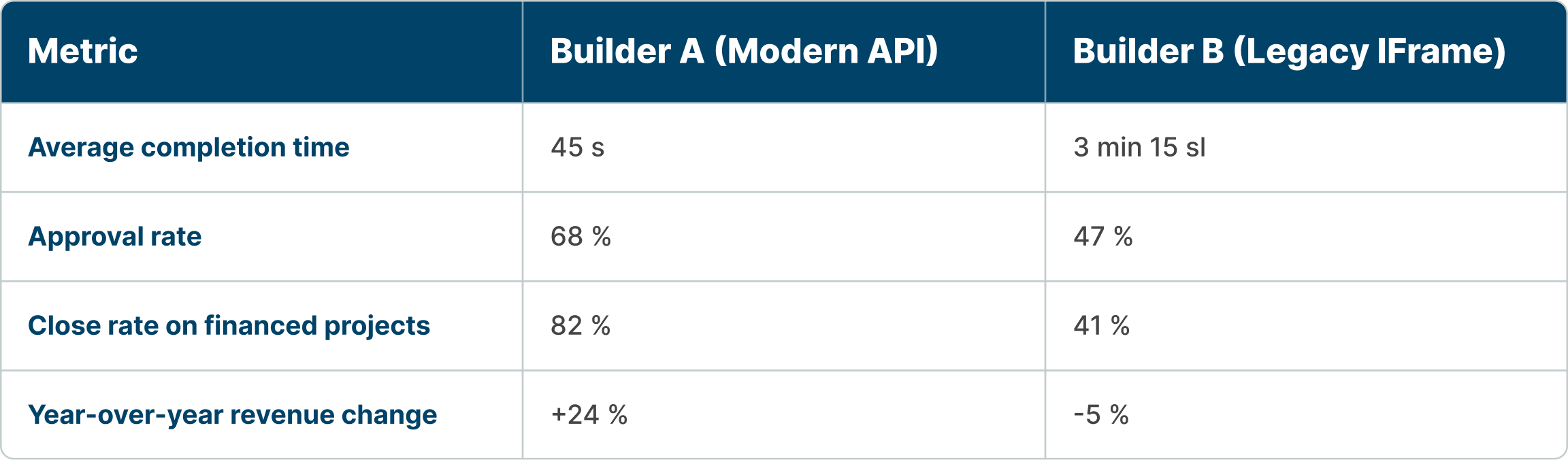

Comparative Case Study

The data illustrate that streamlined, mobile‑optimized workflows deliver materially better conversion and revenue outcomes than older, multi‑step processes. Whether partnering with external home improvement finance companies or building proprietary systems, speed and simplicity remain critical drivers of success.

Conclusion

Conversion data across the e‑commerce and financial‑services sectors demonstrate that speed is a critical determinant of financing success in home‑improvement contexts. Reducing load times, minimizing form complexity, and delivering rapid credit decisions collectively improve approval rates and overall customer satisfaction.

These measures are especially important for Millennials and Generation Z, whose purchasing power and digital expectations will shape the market for years to come.

By adopting the benchmarks and implementation practices outlined above, companies offering contractor financing, including retailers and service providers, can capture a larger share of high‑intent shoppers, improve sales efficiency, and maintain customer trust in an increasingly competitive landscape. Solutions like FinMkt can help deliver mobile-first, high-speed financing experiences that meet modern expectations.